3 Accounting and Finance

Chapter 3 Accounting and Finance

Overview

To be a responsible organization, a firm must know how to manage its books of accounts. In the corporate world, organizations have accounting and audit departments that work on correctly reporting their financial results. Investors and other stakeholders alike read these with a lot of interest. After learning about financial markets in Chapter 2, it is now time to look within. Chapter 3 is based on assets and liabilities, financial statements (Balance sheet and income statement) of a firm and how a financial manager uses these financial statements to make decisions. The most crucial part which will be used subsequently is the statement of cash flows. Cash flows are very important to determine the viability of a new project that the firms' managers propose to undertake.

Learning Objectives

After going through this chapter, students will be able to.

-

Understand details of a balance sheet.

-

Interpret the information from balance sheet.

-

Interpret key data from common size balance sheet

-

Understand the income statement of a firm

- Interpret key data from common size income statement

-

Connect the income statement with cash flows

- Analyze the connection between balance sheet and income statement on the statement of cash flows of a firm

-

Analyze corporate and personal tax rates

-

Deduce marginal and average tax rates

3.1 Financial Statements

Corporations (Businesses) exist to compete in the marketplace and sell their products and services. However, stakeholders (anybody with interest in the firm including shareholders, debtholders, government, suppliers and employees) want to know how corporations are doing in terms of both their sales and profits, and the size of the firm and sources and uses of funds. Accurate measurement of these items is crucial to learn how the firm is changing with time and to identify which strategies are effective. Corporations generate such information through financial statements such as Balance Sheets and Income Statements.

Furthermore, to assess the short-term health and sustenance of a corporation, firms generate statements of cash flow. A startup firm is usually small and may or may not be profitable. So, balance sheets and income statements may not look very promising in the short term. However, investors may still find that the firm is promising because it is generating positive cash flows and will likely accrue income over time. In this chapter, we will explore another phenomenon — a corporation can do business and still not make any profit, but its actions will still affect its cash flow statement. The value in exploring these examples demonstrates the importance of statements of cash flow. We will also study common-size balance-sheet and common-size income statement, which help us compare firms of different sizes (notwithstanding the scale of their operations).

3.2 Balance sheet

A balance sheet is a financial statement of a firm which records the size of the firm. In order to own anything, a firm must raise money. Money can be raised through two sources – debt and equity. Simply put, debt is borrowing and needs to be repaid. Equity is issuance of shares that imply selling part ownership of the firm to new owners (called equity holders or shareholders). Each method brings funds to a corporation. These funds can then be used to purchase machine and equipment or any other means that help a company expand its operations. Sometimes debt or equity is raised to either repay debt or to substitute a debt that is maturing. It is for this reason that professionals in finance discuss assets as uses of funds and issuance of debt or equity as sources of funds. Therefore, sometimes a balance-sheet can also be viewed as “sources” and “uses” of funds.

3.2.1 Assets, Liabilities, and Owners’ Equity

We notice from above; assets and liabilities are part of the balance sheet. Therefore, before we move further, we need to define assets and liabilities. In order to determine if an item is an asset or a liability, the process is simple. Simply observe the relationship of that item with the corporation and see if the corporation is paid from it or if the corporation needs to pay for it. If the corporation is paid from it, then the item is an asset. Else, it is a liability. A simple example is plant and machines possessed by a firm. Selling the plant and machines, the firm will get paid and thus plant and machines are assets. A trickier example is that of bonds purchased by a firm. Effectively the firm is lending money to the issuer of the bond. Breaking the relationship will mean selling the bonds, meaning the firm will get paid thereby implying it is an asset. On the other hand, bonds as an example of a liability would be bonds issued by a company. When we break the relation between company and its own bonds issued, we see that company needs to repay its bondholders. Therefore, these bonds issued are a liability. Same is applicable for any loans that the company took from banks.

Formally, an asset is anything that a firm owns. We saw in chapter 1, assets can be tangible such as plant and equipment or intangible such as patents, trademarks and logos. Tangible assets are touched and felt while intangible assets are present only notionally. It is relatively harder to measure the value of intangible assets because intangible assets are not usually traded in markets and therefore do not have a market value. During the acquisition talks of Spirit airlines in 2022 by JetBlue and Frontier, one negotiating point for the company is the value of the “Spirit” brand and how much a customer would be willing to pay for travelling with a company that has acquired Spirit airlines. This may not be so obvious if the company here provides inferior goods1. However, during the purchase of premium brands, customers tend to associate brand loyalty with certain brands and therefore those brands when sold will have a brand value; this is an example of an intangible asset.

Importantly, owners’ equity is not a liability. A company is not entitled to pay any money to its owners if it does not have it. This becomes important when we discuss liquidation of a company. If a company goes bankrupt, its assets are sold off to other entities in order to raise cash. This cash is then used to pay off all liabilities. Any remaining cash will be distributed equally among all shares to the shareholders. Therefore, owners have this “residual stake” at the liquidation value of a firm.

A balance sheet broadly consists of the above discussed two parts: One part is for assets that displays the possessions of a firm, and the other part displays the total amounts raised from various stakeholders. As discussed above, firms raise capital as the liabilities and owners’ equity. So, the broad categories in a balance sheet are: Assets, Liabilities, and owners’ equity. A balance sheet is a powerful tool to observe the evolution of the size of a corporation and the sources of funds utilized in this evolution. For example, invariably an airline will grow if it purchases aircraft for its fleet rather than leasing for expansion of operations. This increase of assets can be observed in the balance sheet. However, more importantly, we can also find out looking at the liabilities and owners’ equity side how a growth in these assets was funded – through increasing debt or equity. Furthermore, if it leases aircraft then there is no need to raise cash for funding aircraft purchases. However, the airline will have to pay lease, which occurs as an expense in the income statement, which we will study in the next section. Some parts of income statement such as revenue and expenses are not directly reported as part of the balance sheet. (Caveat: lease discussion can be tricky with the new rules on reporting).

3.2.2 Constituents of two sides of a balance sheet

We come back to our discussion on balance sheet. Figure 3.1 below shows some short- and long-term assets and liabilities of a firm. The way this balance sheet is arranged is that assets are listed on the left and liabilities and owners’ equity are on the right. Assets are usually categorized as current or short-term assets and fixed or long-term assets. Usually, short-term assets have a life of less than a year (that is those are either cash or are converted to cash within a year), while long-term assets last for several years. For an airline, fuel is a short-term asset while an aircraft that it owns is a long-term asset. Short- and long-term assets and liabilities are linked with money and capital markets respectively on the balance sheet.

|

Assets |

Liabilities |

|

|

|

|

Current Assets |

Current liabilities |

|

|

|

|

Cash |

Accounts Payable |

|

Short-term investments |

Short-term debt |

|

Accounts receivable |

Other current liabilities |

|

Inventories |

|

|

Other current Assets |

Long-term Liabilities |

|

|

|

|

Long-term Assets |

Long-term debt |

|

|

Other long-term liabilities |

|

Net Plant, property |

|

|

Other Long-term assets |

Total Owners' equity |

|

|

|

|

|

Common stock |

|

|

Retained earnings |

|

|

|

|

Total Assets |

Total Liabilities and OE |

Because liabilities and owners’ equity are used to fund the purchase of assets, it must be noted that the size of total assets must equal the size of total liabilities and owners’ equity. In other words, the balance sheet must be balanced. That is depicted in equation 3.1 below.

Total Assets = Total Liabilities + Owners’ Equity …(3.1)

Total assets are comprised of long- and short-term assets. Assets whose life typically exceeds one year are long-term assets. There are several examples such as plant and machines, value of a building, and in the case of aviation it is the value of aircraft (owned by the airline). These long-term assets are major investments of firms through which firms generate goods and services and run their business. Long -term assets are written off slowly over the age of their life using depreciation. This write-off process can be linear or non-linear and is a topic of an accounting class. But as an asset loses value in balance sheet, either a liability is paid off or owners’ equity decreases to pay off the asset. This process re-establishes the equilibrium between assets on one hand and liabilities and owners’ equity on the other.

Short-term assets are important for maintenance of liquidity and day-to-day operations of a firm. These are usually a part of money markets. Examples are cash, accounts receivable, inventory such as raw materials, intermediate goods, and finished product not yet sold. In case of airlines, short-term assets could include aircraft fuel which is unused, maintenance parts and equipment which is regularly used, and food & other items procured to serve the passengers.

Liabilities are also categorized as short- and long-term liabilities. Short-term liabilities include payables to others for materials purchased, short-term commercial paper borrowings, and bank loans or lines of credit borrowed. Long-term liabilities include funds owed in bank loans and debentures which typically exceed a period of one year.

3.2.3 Balance sheet as a snapshot at a given point in time

There are several ways to represent a balance sheet, and we will discuss three such ways.

First, the most common way is to represent assets first and then liabilities and owners’ equity to represent that Total Assets = Total Liabilities + Owners’ Equity

Second, a market value balance sheet dynamically changes the asset and liability values as their value in real life changes with time. However, this is not the common way of representing a balance sheet. Most long-term assets and liabilities are shown at their acquisition cost (minus any depreciation written off), which can be misleading to investors.

Third, sometimes balance sheets of large and small companies are compared using common size balance sheet, in which all assets and liabilities are divided by size of total assets and represented as a percentage. Size of balance sheet is an attractive way to assess the size of a corporation indiscriminately across sectors – whether it is a bank, an airline or an information technology (IT) company. In particular, for shareholders, it is important to know the size of total assets, the amount of cash (and short-term securities) held, as well as owners’ equity. A balance sheet is a quick source of reference to access this information.

One limitation of balance sheet is that it presents snapshot of a company at any given point in time. However, a company’s business is not static and therefore its balance sheet by definition should not be static. In a simple example below, we will observe how the balance sheet changes with every single business operation of the firm even when the firm is actually not recording sales or making profits. Then we will complicate this chapter by bringing in sales and profits. However, we will first discuss the income statement.

3.3 Income statement and the Statement of cash flows

3.3.1 Income Statement

An income statement is a financial statement that shows revenues a corporation earns and expenses that the corporation makes in producing and selling the goods or services. The difference of revenues and production costs yields operating revenues. When we remove non-operating expenses, such as selling expenses, then we arrive at earnings before interest and taxes (EBIT). When we subtract interest expenses from EBIT, we obtain earnings before taxes (EBT). Finally, we subtract tax expenses to obtain net income or net profit or earnings after taxes (EAT). Net income is very important because investors and shareholders care about how much money is available for their appropriation from business operations of that year (recall that shareholders and owners of a company receive residual profits). Residual profits are distributed on a per share basis, i.e. net profits divided by total shares outstanding = profits per share.

In summary,

Revenue – production cost = operating revenue …(3.2)

Revenue – production cost – selling, general and administrative expenses = EBIT …(3.3)

Or, Operating Revenue – selling, general and administrative expenses = EBIT …(3.4)

Revenue – production cost – selling, general and administrative expenses – Interest Expenses = EBT …(3.5)

Or, EBIT – interest expenses = EBT …(3.6)

Revenue – production cost – selling, general and administrative expenses – Interest Expenses – Taxes = Net Profit …(3.7)

EBT – Taxes = Net Profit …(3.8)

Profit per share = Net Profit/ number of shares outstanding …(3.9)

These equations are summarized in figure 3.2 below:

|

Revenue |

|

Minus |

|

Cost of goods sold |

|

Depreciation |

|

Selling, general, admn exp |

|

Other exp |

|

Equals |

|

Operating income |

|

(+) Other income (-) other expense |

|

Equals |

|

EBIT |

|

(-) Interest expense |

|

Equals |

|

EBT(Taxable income) |

|

(-) Taxes |

|

Equals |

|

EAT/ Net Income/ Net Profit |

Items that are common between income statement and the balance sheet are depreciation, net income or net profits or EAT. Depreciation expense accumulates over time and erodes the value of plant and machines to reduce size of assets. Similarly, profit after taxes increase the size of owners’ equity. We will see the connections between these items in income statement and balance sheet later in this chapter after we finish discussing balance sheet and income statements separately.

However, there are some problems in interpreting income statement. The biggest problem is that not all profits are earned in cash. Cash sometimes moves very differently from how a company earns profits. For example, when a loss-making company takes a huge loan for its expansion its cash flows would be positive and yet profits would be negative. We will discuss such impacts in detail when we study the statement of cash flows.

3.3.2 Cash Flows

One major problem with the measurement of net income is that net income doesn’t necessarily represent the cash generated by the firm – actually cash generated by the firm and net income can be very different. Cash flow is defined as the difference of cash generated and cash used. Cash can be generated by non-business (non-operating) activities. Cash can be used for non-operating activities too. Let us recall the definition of accounts receivable: when we make a credit sale, accounts receivable increase. If a company makes credit sales (and hence generates no cash) but pays off all costs required to generate the product with cash: this is an example of non-cash operating activity being funded by a cash operating activity. However, this is a potentially problematic situation for the company because then at the limit, the company will not have cash left for its day-to-day operations. Therefore, cash flows are an important component that a company and investors must always take seriously. It is said that in 2008 one reason why Lehmann Brothers, the great investment bank, collapsed is the mismanagement of cash flows. Lehmann Brothers did not have the liquidity to tide over its day-to-day operations even though it had potential buyers of its assets: Barclays Plc., which ultimately acquired all the Lehmann North America operations. Hence, the statement of cash flows is an extremely important statement for investors. Every quarter when a company reports its results, not only are its profits per share important, but equally important are its cash flow per share. As we discussed before, profit per share is defined as the net profit divided by total shares outstanding. Profit per share gives an indication of total margin earned by the company for a shareholder. Similarly, cash flow per share is the net cash generated divided by total shares outstanding. Cash flow per share gives an indication of liquidity generation of the company per unit share. It is important to compare cash flow per share with profit per share because in the short term, a company’s liquidity is very important in determining its ability to pay off its short-term liabilities. Therefore, profit per share is important in noticing how the company would do in a longer run and cash flow per share is important in checking how the company would do in the short run.

3.3.3. Working example: Balance sheet

Now, we will look at a simple example of starting a coffee shop and how it affects a company’s balance sheet, income statement, and cash flows.

Suppose Ms. Cici wants to start a coffee shop with her $ 700. However, she is very ambitious and thinks she can convert it into a large multinational corporation called Barstucks Inc. But right now, she wants to start small. So, she gives $ 700 to Barstucks to create owners’ equity worth $ 700. Let us analyze the effects of following steps on its balance sheet below.

Step 1:

Barstucks at its end now has cash worth $ 700 but owner’s equity is $ 700. This is seen as in table 3.1 below.

|

Assets |

|

Liabilities |

||

|

|

|

|

|

|

|

Current Assets |

$ 700 |

|

Current liabilities |

$ - |

|

|

|

|

|

|

|

Cash |

$ 700 |

|

|

|

|

|

|

|

Total Owners' equity |

$ 700 |

|

|

|

|

|

|

|

|

|

|

Common stock |

$ 700 |

|

|

|

|

|

|

|

Total Assets |

$ 700 |

|

Total Liabilities and OE |

$ 700 |

Step 2:

CEO Ms. Cici now decides to buy a machine for $ 500. As a result, its cash decreases to $ 200 as in Table 3.2 below.

|

Assets |

|

Liabilities |

||

|

|

|

|

|

|

|

Current Assets |

$200 |

|

Current liabilities |

$0 |

|

|

|

|

|

|

|

Cash |

$200 |

|

|

|

|

|

|

|

|

|

|

Long-term Assets |

$500 |

|

Long-term Liabilities |

$0 |

|

|

|

|

|

|

|

Net Plant, property |

$500 |

|

|

|

|

|

|

|

Total Owners' equity |

$700 |

|

|

|

|

|

|

|

|

|

|

Common stock |

$700 |

|

|

|

|

|

|

|

Total Assets |

$700 |

|

Total Liabilities and OE |

$700 |

Step 3:

Next, she buys raw materials such as coffee, cream, sugar etc. to start business operations. Therefore, its raw material inventory increases by $100. However, she buys it on credit. Therefore, her liabilities also increase by $ 100 (accounts payable). This leads to expansion of its balance sheet from $ 700 to $ 800 as in Table 3.3 below.

Step 4:

Next she converts 10% of her raw material into 10 coffees, whose value is approximate $1 each. This is depicted in Barstucks’ balance sheet under Inventories (finished goods) in Table 3.4 as follows:

|

Assets |

|

Liabilities |

||

|

|

|

|

|

|

|

Current Assets |

$300 |

|

Current liabilities |

$100 |

|

|

|

|

|

|

|

Cash |

$200 |

|

Accounts Payable |

$100 |

|

Short-term investments |

|

|

Short-term debt |

|

|

Accounts receivable |

|

|

Other current liabilities |

|

|

Inventories (raw materials) |

$90 |

|

|

|

|

Inventories (finished goods) |

$10 |

|

|

|

|

|

|

|

|

|

|

Long-term Assets |

$500 |

|

Long-term Liabilities |

$0 |

|

|

|

|

|

|

|

Net Plant, property |

$500 |

|

Long-term debt |

|

|

Other Long-term assets |

|

|

Other long-term liabilities |

|

|

|

|

|

|

|

|

|

|

|

Total Owners' equity |

$700 |

|

|

|

|

|

|

|

|

|

|

Common stock |

$700 |

|

|

|

|

Retained earnings |

|

|

|

|

|

|

|

|

Total Assets |

$800 |

|

Total Liabilities and OE |

$800 |

Step 5:

Note that income statement has not been affected in steps 1 through 4, because no sales have been made.

However, that changes in the next step /step 5 /Table 3.5. Ms. Cici finally makes a sale. She sells those ten coffees for $25 on credit. This now decreases her inventory of finished goods and increases her accounts receivable. This is now depicted in Table 3.5 below.

|

Assets |

|

Liabilities |

||

|

|

|

|

|

|

|

Current Assets |

$315 |

|

Current liabilities |

$100 |

|

|

|

|

|

|

|

Cash |

$200 |

|

Accounts Payable |

$100 |

|

Short-term investments |

|

|

Short-term debt |

|

|

Accounts receivable |

$25 |

|

Other current liabilities |

|

|

Inventories (raw materials) |

$90 |

|

|

|

|

Inventories (finished goods) |

$0 |

|

|

|

|

|

|

|

|

|

|

Long-term Assets |

$500 |

|

Long-term Liabilities |

$0 |

|

|

|

|

|

|

|

Net Plant, property |

$500 |

|

Long-term debt |

|

|

Other Long-term assets |

|

|

Other Long-term liabilities |

|

|

|

|

|

|

|

|

|

|

|

Total Owners' equity |

$700 |

|

|

|

|

|

|

|

|

|

|

Common stock |

$700 |

|

|

|

|

Retained earnings |

|

|

|

|

|

|

|

|

Total Assets |

$815 |

|

Total Liabilities and OE |

$800 |

From Table 3.5 above, we can notice that Assets now exceed liabilities. However, this is a problem – and the problem is that balance sheet is now unbalanced. While the assets side shows $815, the liabilities and OE side shows $800.

Step 6:

Ms. Cici actually made a sale (even though not in cash). This is not correctly depicted in the balance sheet. We will learn later that this is recorded in the income statement. For now, the most important part is that revenue minus cost is $ 15, which is the difference between the assets and liabilities and OE. These $ 15 of profits are recorded as retained earnings. Another aspect to note is that the company made sales and profits but not cash! Let us correct the balance sheet in Table 3.6 below by $ 15 to reflect on the increase in owners’ equity. Notice the increase in retained earnings in table 3.6 below, where the increase is attributed to profits earned in the period.

|

Assets |

|

Liabilities |

||

|

|

|

|

|

|

|

Current Assets |

$315 |

|

Current liabilities |

$100 |

|

|

|

|

|

|

|

Cash |

$200 |

|

Accounts Payable |

$100 |

|

Short-term investments |

|

|

Short-term debt |

|

|

Accounts receivable |

$25 |

|

Other current liabilities |

|

|

Inventories (raw materials) |

$90 |

|

|

|

|

Inventories (finished goods) |

$0 |

|

|

|

|

|

|

|

|

|

|

Long-term Assets |

$500 |

|

Long-term Liabilities |

$0 |

|

|

|

|

|

|

|

Net Plant, property |

$500 |

|

Long-term debt |

|

|

Other Long-term assets |

|

|

Other long-term liabilities |

|

|

|

|

|

|

|

|

|

|

|

Total Owners' equity |

$715 |

|

|

|

|

|

|

|

|

|

|

Common stock |

$700 |

|

|

|

|

Retained earnings |

$15 |

|

|

|

|

|

|

|

Total Assets |

$815 |

|

Total Liabilities and OE |

$815 |

Step 7:

Next Ms. Cici wants to pay suppliers $50 cash. To do this, her cash decreases to $150 and Account Payables decreases to $50 as seen in Table 3.7 below. We can also see that the balance sheet has shrunk.

|

Assets |

|

Liabilities |

||

|

|

|

|

|

|

|

Current Assets |

$265 |

|

Current liabilities |

$50 |

|

|

|

|

|

|

|

Cash |

$150 |

|

Accounts Payable |

$50 |

|

Short-term investments |

|

|

Short-term debt |

|

|

Accounts receivable |

$25 |

|

Other current liabilities |

|

|

Inventories (raw materials) |

$90 |

|

|

|

|

Inventories (finished goods) |

$0 |

|

|

|

|

|

|

|

|

|

|

Long-term Assets |

$500 |

|

Long-term Liabilities |

$0 |

|

|

|

|

|

|

|

Net Plant, property |

$500 |

|

Long-term debt |

|

|

Other Long-term assets |

|

|

Other long-term liabilities |

|

|

|

|

|

|

|

|

|

|

|

Total Owners' equity |

$715 |

|

|

|

|

|

|

|

|

|

|

Common stock |

$700 |

|

|

|

|

Retained earnings |

$15 |

|

|

|

|

|

|

|

Total Assets |

$765 |

|

Total Liabilities and OE |

$765 |

Step 8:

Next, she receives $ 25 from her customers. So, the cash of Barstucks increases and receivables decrease by $ 25 as seen in Table 3.8 below.

|

Assets |

|

Liabilities |

||

|

|

|

|

|

|

|

Current Assets |

$265 |

|

Current liabilities |

$50 |

|

|

|

|

|

|

|

Cash |

$175 |

|

Accounts Payable |

$50 |

|

Short-term investments |

|

|

Short-term debt |

|

|

Accounts receivable |

$0 |

|

Other current liabilities |

|

|

Inventories (raw materials) |

$90 |

|

|

|

|

Inventories (finished goods) |

$0 |

|

|

|

|

|

|

|

|

|

|

Long-term Assets |

$500 |

|

Long-term Liabilities |

$0 |

|

|

|

|

|

|

|

Net Plant, property |

$500 |

|

Long-term debt |

|

|

Other Long-term assets |

|

|

Other long-term liabilities |

|

|

|

|

|

|

|

|

|

|

|

Total Owners' equity |

$715 |

|

|

|

|

|

|

|

|

|

|

Common stock |

$700 |

|

|

|

|

Retained earnings |

$15 |

|

|

|

|

|

|

|

Total Assets |

$765 |

|

Total Liabilities and OE |

$765 |

Step 9:

Suppose instead of receiving $25 from customers, Ms. Cici decides to borrow another $ 700 to start another shop. This is seen in Table 3.9 below. Notice that on asset side, the cash has increased by $700; in the liability side, long-term liability has increased by $700. Overall, the size of the balance sheet has gone up by $700.

|

Assets |

|

Liabilities |

||

|

|

|

|

|

|

|

Current Assets |

$965 |

|

Current liabilities |

$50 |

|

|

|

|

|

|

|

Cash |

$850 |

|

Accounts Payable |

$50 |

|

Short-term investments |

|

|

Short-term debt |

|

|

Accounts receivable |

$25 |

|

Other current liabilities |

|

|

Inventories (raw materials) |

$90 |

|

|

|

|

Inventories (finished goods) |

$0 |

|

|

|

|

|

|

|

|

|

|

Long-term Assets |

$500 |

|

Long-term Liabilities |

$700 |

|

|

|

|

|

|

|

Net Plant, property |

$500 |

|

Long-term debt |

$700 |

|

Other Long-term assets |

|

|

Other long-term liabilities |

|

|

|

|

|

|

|

|

|

|

|

Total Owners' equity |

$715 |

|

|

|

|

|

|

|

|

|

|

Common stock |

$700 |

|

|

|

|

Retained earnings |

$15 |

|

|

|

|

|

|

|

Total Assets |

$1,465 |

|

Total Liabilities and OE |

$1,465 |

Next, we will look at common size balance sheet.

3.3.4 Income statement

Let us see the effect of these transactions on the income statement described above.

Since sales made was for $ 25 and the cost of these transactions was $ 10. Assuming no other expenses were made in this period, the income statement looks as in table 3.10 below.

|

|

Income statement |

|

Revenue |

25 |

|

Cost of goods sold |

10 |

|

Depreciation |

|

|

Selling, general, admn exp |

|

|

Other exp |

|

|

|

|

|

Operating income |

15 |

|

Other income |

|

|

|

|

|

EBIT |

15 |

|

Interest expense |

0 |

|

|

|

|

Taxable income |

15 |

|

Taxes |

0 |

|

|

|

|

Net Income |

15 |

3.3.5 Common size balance sheet

Common size balance sheet is balance sheet expressed in percentage. All items in balance sheet are expressed as percent of total assets. Using this method, let us translate Table 3.1 into a common size balance sheet. In table 3.1, there are just two items. On assets side, there is cash = $ 700, while on Liabilities and OE side, there is OE = 700. Both are 100% percent of total assets. This is further elaborated in detail in table 3.11 below. Table 3.11 below represents contents of table 3.1 and derives common size balance sheet in columns on the right. Titles are also displayed to guide a reader through these.

|

|

Assets |

|

|

Liabilities |

|||||

|

|

Level, $ |

Percentage |

|

|

Level, $ |

Percentage |

|||

|

Current Assets |

700 |

100% |

|

Current liabilities |

$ 0 |

$ - |

|||

|

|

|

|

|

|

|

|

|||

|

Cash |

700 |

100% |

|

Accounts Payable |

|

|

|||

|

Short-term investments |

|

|

|

Short-term debt |

|

|

|||

|

Accounts receivable |

|

|

|

Other current liabilities |

|

|

|||

|

Inventories |

|

|

|

|

|

|

|||

|

Other current Assets |

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|||

|

Long-term Assets |

$ 0 |

$ - |

|

Long-term Liabilities |

$ 0 |

$ - |

|||

|

|

|

|

|

|

|

|

|||

|

Net Plant, property |

|

|

|

Long-term debt |

|

|

|||

|

Other Long-term assets |

|

|

|

Other long-term liabilities |

|

|

|||

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

Total Owners' equity |

$ 700 |

100% |

|||

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

Common stock |

$ 700 |

100% |

|||

|

|

|

|

|

Retained earnings |

|

|

|||

|

|

|

|

|

|

|

|

|||

|

Total Assets |

$ 700 |

100% |

|

Total Liabilities and OE |

$ 700 |

100% |

|||

Let us now translate Table 3.2 into common size balance sheet in table 3.12 below.

|

Assets |

|

Liabilities |

||||

|

|

Level, $ |

Percentage |

|

|

Level, $ |

Percentage |

|

Current Assets |

$ 200 |

29% |

|

Current liabilities |

$ 0 |

0% |

|

|

|

|

|

|

|

|

|

Cash |

$ 200 |

29% |

|

Accounts Payable |

|

|

|

Short-term investments |

|

|

|

Short-term debt |

|

|

|

Accounts receivable |

|

|

|

Other current liabilities |

|

|

|

Inventories |

|

|

|

|

|

|

|

Other current Assets |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Long-term Assets |

$ 500 |

71% |

|

Long-term Liabilities |

$ 0 |

0% |

|

|

|

|

|

|

|

|

|

Net Plant, property |

|

71% |

|

Long-term debt |

|

|

|

Other Long-term assets |

|

|

|

Other long-term liabilities |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total Owners' equity |

$ 700 |

100% |

|

|

|

|

|

|

|

|

|

|

|

|

|

Common stock |

$ 700 |

100% |

|

|

|

|

|

Retained earnings |

|

|

|

|

|

|

|

|

|

|

|

Total Assets |

$ 700 |

100% |

|

Total Liabilities and OE |

$ 700 |

100% |

Next, let us create an income statement based on the statement described in table 3.10. We will observe the effect of all these transactions on the income statement. Recall that it was only in step 5 (Fig 3.5) that we made coffee sales. As we see in Table 3.13, we only apply $10 of cost to the revenue of $25, even though we spent $ 100 in raw materials. This is called accrual in accounting. We only “accrue” that part of cost to the revenue that was spent to produce that amount of goods. The rest of “cost” will sit in the balance sheet as “assets.” This is the first connection between balance sheet and income statement. The second connection is the addition of $ 15 (profit) as retained earnings in owners’ equity.

|

|

Income statement |

Common size |

|

Revenue |

25 |

100% |

|

Cost of goods sold |

10 |

40% |

|

Depreciation |

|

0% |

|

Selling, general, admn exp |

|

0% |

|

Other exp |

|

0% |

|

|

|

|

|

Operating income |

15 |

60% |

|

Other income |

|

0% |

|

|

|

|

|

EBIT |

15 |

60% |

|

Interest expense |

0 |

0% |

|

|

|

|

|

Taxable income |

15 |

60% |

|

Taxes |

0 |

0% |

|

|

|

|

|

Net Income |

15 |

60% |

3.4 Cash Flow Statement

Investors in a company are interested in not only profits but also cash flows. If a company cannot generate cash flows, there is a problem with its short- and medium-term liquidity. This is important from the perspective of paying off its obligations, particularly to short term creditors and suppliers. While there is no magic formula for how much cash flow should be generated, cash flow generation is broadly seen as a benchmark of healthy liquidity. Cash flow statement is composed of cash flows from investing, operating and financing.

Cash flows from operations are the effects of various operating activities such as acquisition of raw materials, money spent in making sales, receipt of sales revenues etc. These are all activities linked with running day-to-day business.

Cash flows from investing activities are the directly related to acquisition and/ or sale of fixed and long-term assets such as plant and machines, investments through merchant banking units such as purchase of bonds and shares and also acquisition of other firms.

Cash flows from financing activities are directly related to creating sources of funds either through debt or equity routes such as issue of bonds or stock or taking new term loan.

Among these three, operating activities are usually short term in nature, while investing and financing activities are more long term in nature.

3.4.1 Cash flows from operations

So far, we have seen how to create, understand and analyze balance sheet, income statement and common size variations. Now, we will see the statement of cash flows. As may be recalled, our cash position keeps changing as long as there are transactions in cash. Some items of the cash flow statement are revenue, cost of goods sold, change in inventories, change in accounts receivable and change in accounts payable. Let us discuss each of them individually.

When we sell goods (i.e. generate a revenue), it is expected that our cash position goes up. This was illustrated by Ms. Cici selling her coffees. In our example, although the first sale made was based on credit, sales are generally made in cash payments. Additionally, for every dollar of sales, we must take into consideration the money spent on purchasing raw materials or other items. The corresponding cash spent for the acquisition of inventory of raw materials toward finished goods used for making those sales decreases our cash position, so we can see a minus sign.

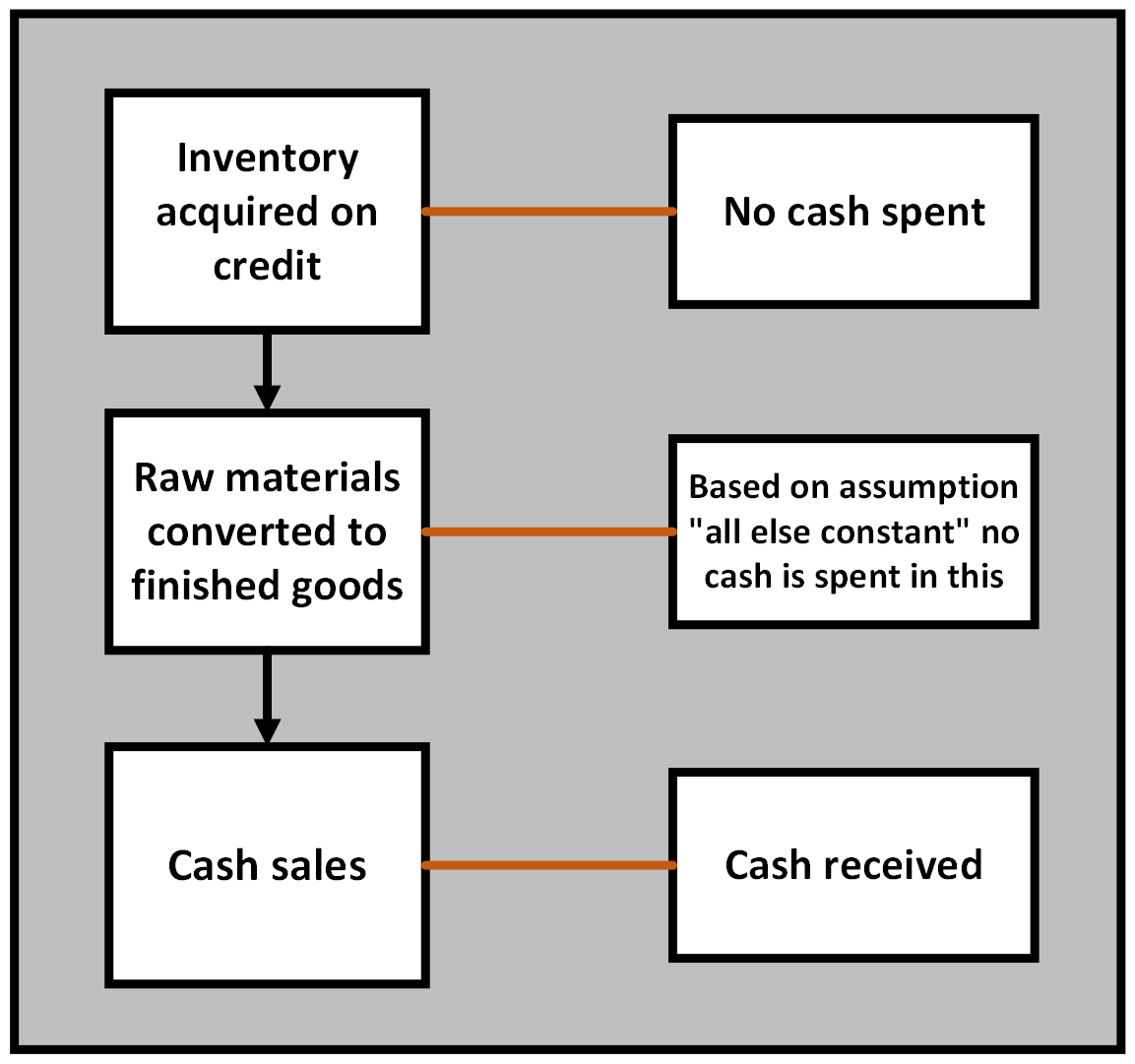

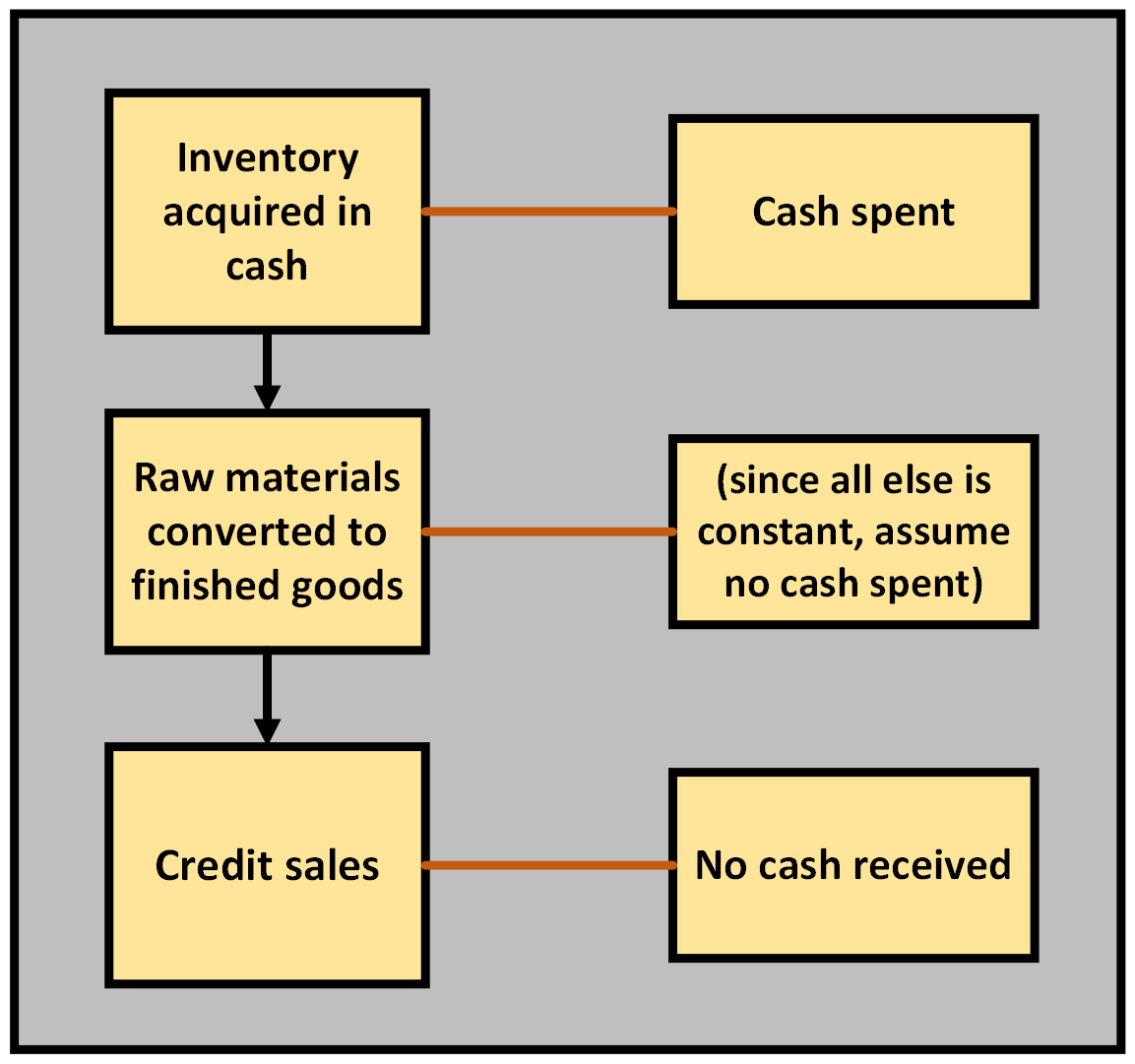

Next, if accounts payable increase (as it did when Ms. Cici bought supplies using credit), then all else constant, we must have bought some goods, produced them and sold them for cash. Hence, our cash goes up – such transactions bring change in accounts payable a positive sign or a direct proportionality with cash flows. This is further illustrated in figure 3.3 below.

Another simple way to look at this is we can only pay down accounts payable if our cash position goes down. In summary, , all else constant, if accounts payable go up, so does cash and vice versa.

On the other hand, accounts receivable have opposite effect. If accounts receivable increase (as it did when Ms. Cici sold her coffees to customers paying credit), then all else constant, we must have made a sale on credit for which we procured raw materials and undertook other expenses in cash. Thus, all else constant, accounts receivable going up leads to decrease in cash, and vice versa, thereby demonstrating an inversely proportional relationship between accounts receivable and cash. This is illustrated in figure 3.4 below.

A simple way to look at this inverse proportionality is that when accounts receivable go down, the only way these can decrease is when someone makes a payment2. Hence cash goes up.

All the above discussion is reflected in the cash flow statement, which reads as revenue minus cost of goods sold minus change in inventories minus change in accounts receivable plus change in accounts payable. First let us discuss the ceteris paribus effects:

- ↑ sales = ↑ cash flow (direct proportionality)

- ↑ cost of goods sold = ↓ cash flow (inverse proportionality)

- ↑ inventories = ↓ cash flow (inverse proportionality)

- ↓ accounts receivable = ↑ cash flow (inverse proportionality)

- ↓ accounts payable = ↓ cash flow (direct proportionality)

Summary of the overall effects of balance sheet and income statement items on cash flow are as in equation 3.10 below.

Cash flow = + sales – COGS – [latex]\Delta[/latex]Inv – [latex]\Delta[/latex]AR + [latex]\Delta[/latex]AP …(3.10)

Table 3.14 below describes in detail the cash flows surrounding each activity we performed in the coffee shop across five periods:

| Period | 0 | 1 | 2 | 3 | 4 | 5 |

|

Sales ($) |

0 | 0 | 25 | 0 | 0 | |

|

- [latex]\Delta[/latex]Accounts Receivable |

0 | 0 | 25 | 0 | -25 | |

|

+ [latex]\Delta[/latex]Accounts payable |

100 | 0 | 0 | -50 | 0 | |

|

- Cost of Goods Sold |

0 | 0 | 10 | 0 | 0 | |

|

- [latex]\Delta[/latex] in Inventories |

-100 | 0 | -10 | 0 | 0 | |

|

Net Cash Flow (change in cash flow) |

0 | 0 | 0 | -50 | 25 | |

|

Calculation |

+100-100 | 0 | 25-25-10-(-10) | +(-50) | -(-25) | |

|

Cash position |

200 | 200 | 200 | 200 | 150 | 175 |

Actions from the table are as follows:

- In period 1, we procured inventories (worth $ 100) using credit. Hence both inventories and accounts payable increase and cancel each other as seen in the row “calculation”.

- In period 2, we simply make 10 coffees (each using $ 1 of inventories). So, there is no change in cash position.

- In period 3, we sell those 10 coffees (costing $ 10) for $ 25 on credit, which creates sales and cost of goods sold, but also decreases inventory of finished goods and increases accounts receivable. Thus, there is no change in cash position.

- In period 4, we pay down payables worth $ 50, which decreases cash.

- In period 5, we receive cash against accounts receivable (worth $ 25). So, accounts receivable decreases and cash increases.

As can be seen from above, cash flow is not necessarily dependent on income statement. Further cash flow is an important consideration for investors because only available cash and not profits determine how much money would be distributed as dividends to shareholders/ owners of the company, which in turn determines the stock price. Cash flow position also governs how much money is available for a company to make new investments.

Details of the above table are discussed in this video.

3.4.2 Cash flows from Investing and Financing

In the above case, Barstucks could not generate enough cash to start a second shop from its profits from regular operations. Therefore Ms. Cici had to make a hard decision – that of taking a bank loan (borrowing) to create a second shop. We see that the first shop was created using owners’ equity. However, the second shop was created using debt. Debt and equity are two ways a company can expand. However, a company’s obligations to its lenders are different from its owners. As seen in the income statement interest expense is paid first. Then dividend distributions are done after paying taxes. Dividends are typically paid if net profits are positive. Sometimes, firms may borrow money to pay dividends.

Broadly speaking, cash flows are affected by operating activities, investing activities and financing activities. In the above example, sale of coffees produced positive cash flow net of raw material costs (operating activities). In the above example, when new machine was purchased, new investment was made and therefore cash decreased. Lastly, when Barstucks raised money from owners or lenders (Ms. Cici’s $ 700 and then bank loan of $ 700), its cash position went up and these are called financing activities.

Change in Cash flow = Cash flow from operations + cash flows from investing activities + cash flows from financing activities ...(3.11)

We know that change in cash flow is ending balance minus beginning balance. Therefore, equation 3.11 can be rewritten as:

Ending cash balance = Beginning cash balance + Cash flow from operations + cash flows from investing activities + cash flows from financing activities ...(3.12)

3.5 Taxation and tax rates

In the US, prior to 2017 corporate tax rates worked in a similar way as personal tax rates. There were brackets for net income and for every bracket, there is a tax rate. There are tax brackets for personal income taxes.

Illustration of marginal and average tax rate for variable tax rates for different income categories.

Suppose the tax rates are as follows:

|

Income bucket or range |

tax rate |

|

0 – 100 |

5% |

|

101 – 200 |

10% |

If corporation A earns $ 100 in income, then it will pay $ 5 in tax.

If corporation B earns $ 165 in income, then it will pay $ 5 in tax on the first $ 100 and 10% on the remaining income (165 – 100 = $ 65). This will be 10% of 65 or $ 6.5. Total tax liability will be $ 5 + $ 6.5 = $ 11.5.

The rates of 5% on first $ 100 and 10% on the next $ 65 are respectively called marginal tax rates for each bucket. The average tax rate for the corporation is $ 11.5/ $ 165 = 6.96%.

In the US for the tax year beginning January 1, 2018, the tax rate has become a flat 21%. So, whether a corporation earns $ 100 or $ 1000, their marginal and average tax rate will be 21% (i.e. $ 21 or $ 210 respectively).

Summary

In this chapter, we analyzed balance sheet and income statement of a firm; looked at different types of balance sheet (common size, market value and book value) and types of income statements (periodic, actual and common size). There was a discussion of profits vs cash flows. Cash flows are very important to a financial manager because illiquidity hampers the efficient functioning of a firm. More importantly, from common size financial statements, we learned that we can actually compare two unequally sized firms with each other (refer to the video below). In other words, taking ratios and comparing for different firms either in a given sector or in an industry helps us analyze various metrics across firms such as liquidity, efficiency, profitability etc. This is seen in the next chapter.

Resources

Self Assessment

This self assessment can help you check your growing knowledge from this chapter. You can take the self-assessment as many times as you would like to check your understanding.

Chapter 3 part 1 Assessment

Chapter 3 part 2 Assessment

Chapter 3 part 3 Assessment

Short Answers and Activities

These activities will help you begin applying concepts in this chapter:

- Activity 3.1 Instructions

- Activity 3.2 Instructions

- Blank Excel file:

- Please fill out green cells only

- Activity 3.1 and 3.2 Chapter 3 Chapter-3-Activity-3.1-and-3.2-blank v2

- Activity 3.3 Instructions: Please create common size income statement

- Blank Excel file:

- Please fill out green cells only

- Activity 3.3 Chapter 3 Activity 3.3 blank

Anybody with interest in the firm including shareholders, debtholders, government, suppliers, and employees.

Supply or distribute.

Physical property that can be touched and have a finite or discrete value.

Asset that lacks physical substance.

Any resource owned or controlled by a business or an economic entity.

Legally binding obligations that are payable to another person or entity.

The right owners have to all of the assets that pertain to their business.

Assets that have a life of less than a year.

Assets that last for several years.

Record that shows revenues a corporation earns and costs that it spends.

The difference of cash generated and cash used.